June 20, 2025

While the stock market continues to remain elevated and just a few percentage points off all-time highs (S&P 500), the economy also appears to continue to chug along. A lot of the noise of tariffs that caused volatility earlier in the year has dissipated for now as trade negotiations continue. That can obviously change in a hurry. Many that were calling for imminent recession back in April have backed off that call. It seems the market is getting back into its mode of climbing the wall of worry. We’ve had tensions overseas continuing to rise. So far, the bombs being dropped in the Middle East haven’t had much effect on the stock market. Even the recent Federal Reserve meeting this week was met with minimal volatility as they kept their benchmark interest rate the same.

While GDP (gross domestic product) in Q1 came in slightly negative, projections for Q2 show a rebound. The Federal Reserve Bank of Atlanta’s GDPNow model shows an estimated 3.4% increase currently for Q2. U.S. company’s reactions to tariffs and front-running with imports in Q1 were the biggest cause for the negative reading. The reverse effect of that with lower imports in Q2 will most likely be the main cause for the rebound. Normally, though consumer spending will be the most important factor to watch, as the large majority of our GDP comes from consumption.

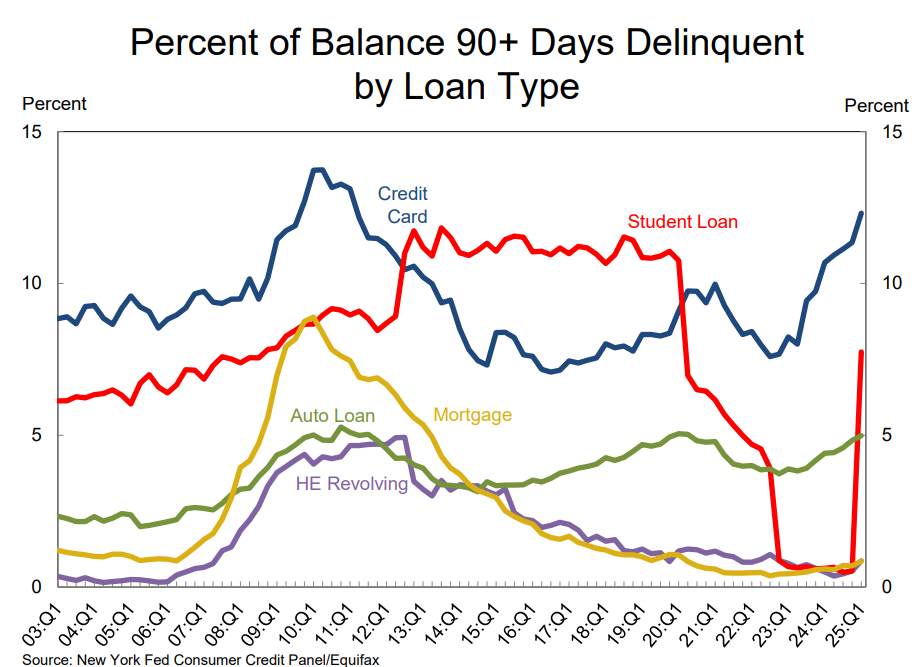

Consumers for the most part have remained resilient over the last few years despite high inflation. One concern though is that they’ve racked up a lot of debt in the process to pay for it. Credit card debt has been at all-time highs for a couple of years now. That by itself isn’t necessarily a concern as credit card usage has never been more prevalent and a large number of households pay it off every month. The concern would be households not paying it off every month and eventually becoming delinquent on payments. The chart below illustrates how this has continued to rise.

Credit card delinquency is reaching levels not seen since the depths of the great recession. Same with auto loan delinquency. The big change in this chart recently is the student loan delinquency. Missed federal student loan payments were allowed to go unreported to credit bureaus through the end of 2024. Repayments resumed in September 2023 but a one-year “on-ramp” period prevented missed payments from affecting credit reports. With that one-year period being up it caused delinquencies to surface in Q1 data for this year and is expected to continue to increase.

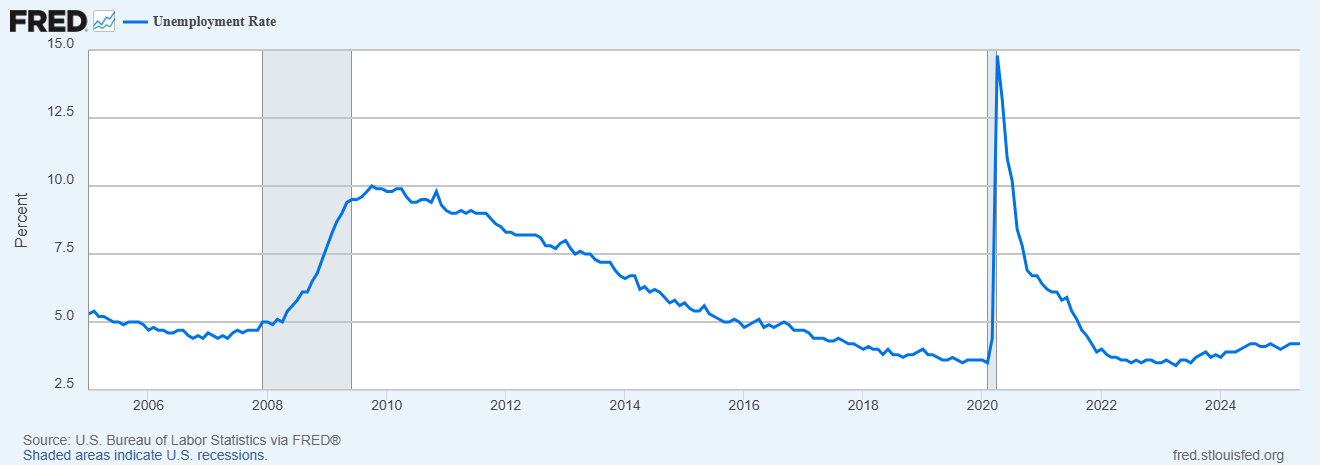

The fact that this is occurring in the backdrop of historically low unemployment is concerning. Delinquency rates on credit cards and auto loans are reaching levels last seen when unemployment was nearly 10%. We currently sit at 4.2% as the chart below illustrates. What would happen if unemployment began to go up and started to reach 6% or more? Delinquency rates would most likely reach levels not seen in modern times. This would obviously not just affect consumer spending that our economy relies on, but many banks as well.

Jobs data will be important to watch moving forward with this backdrop. Initial unemployment claims and continued unemployment claims have ticked up some recently, but are not signaling an immediate slowdown. The number of job openings has been trending down since 2022, but have somewhat stabilized this year near levels seen in 2018 and 2019.

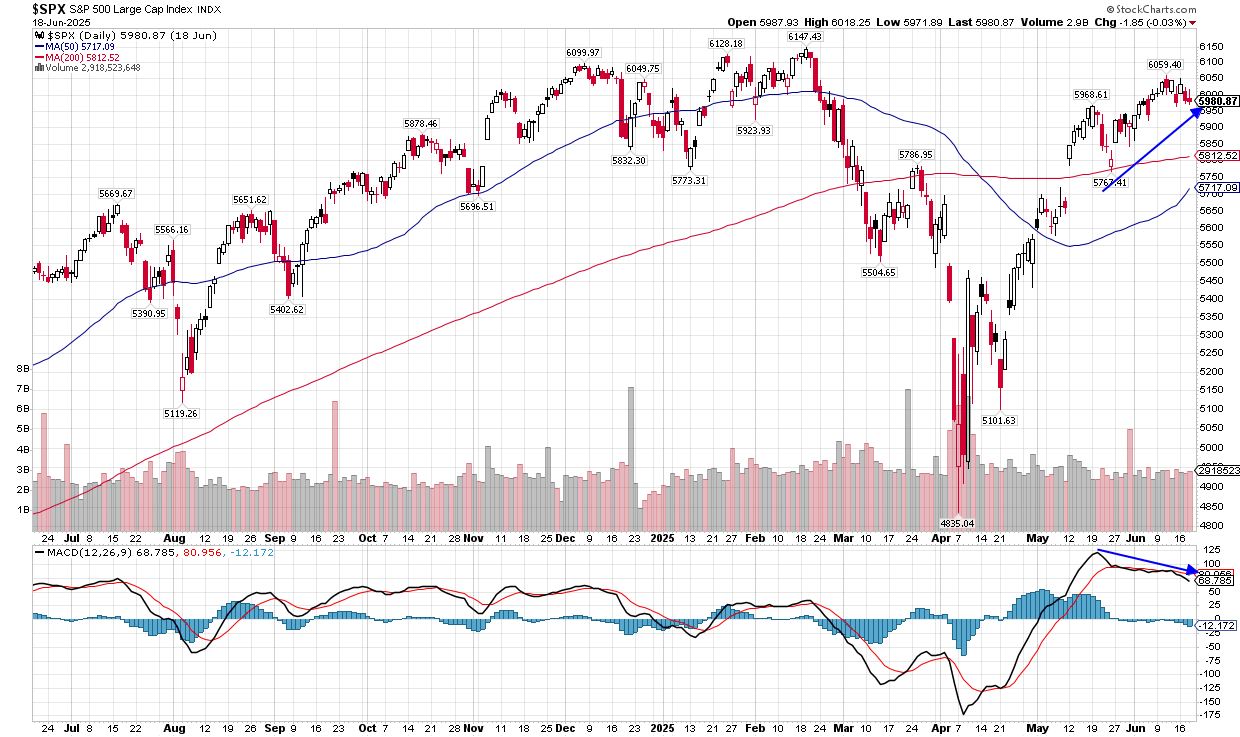

While there is evidence that consumers are getting stretched, that won’t necessarily affect the stock market on a day-to-day basis. The bounce back from the April lows has been quite impressive and as mentioned, the S&P 500 is not far off its all-time high from this past February. It has blown past some of the resistance levels I was watching but has begun to stall a bit. There is also some negative divergence with what price has done since the middle of May in comparison to some of its momentum indicators.

The market taking a breather soon would make sense and how that plays out will be important for how the rest of the year may go. A drop into support that holds can set up for a continued uptrend through 2025 into 2026. One that does not hold support can set up more fireworks like we saw earlier in the year and create a continued choppy and volatile market through the end of the year. Support levels will come in the 5,500-5,800 region as that is where the market began to initially bounce from back in March. Markets also like to fill gaps, and we have one from the jump higher in May with the bottom of gap support right around 5,700.

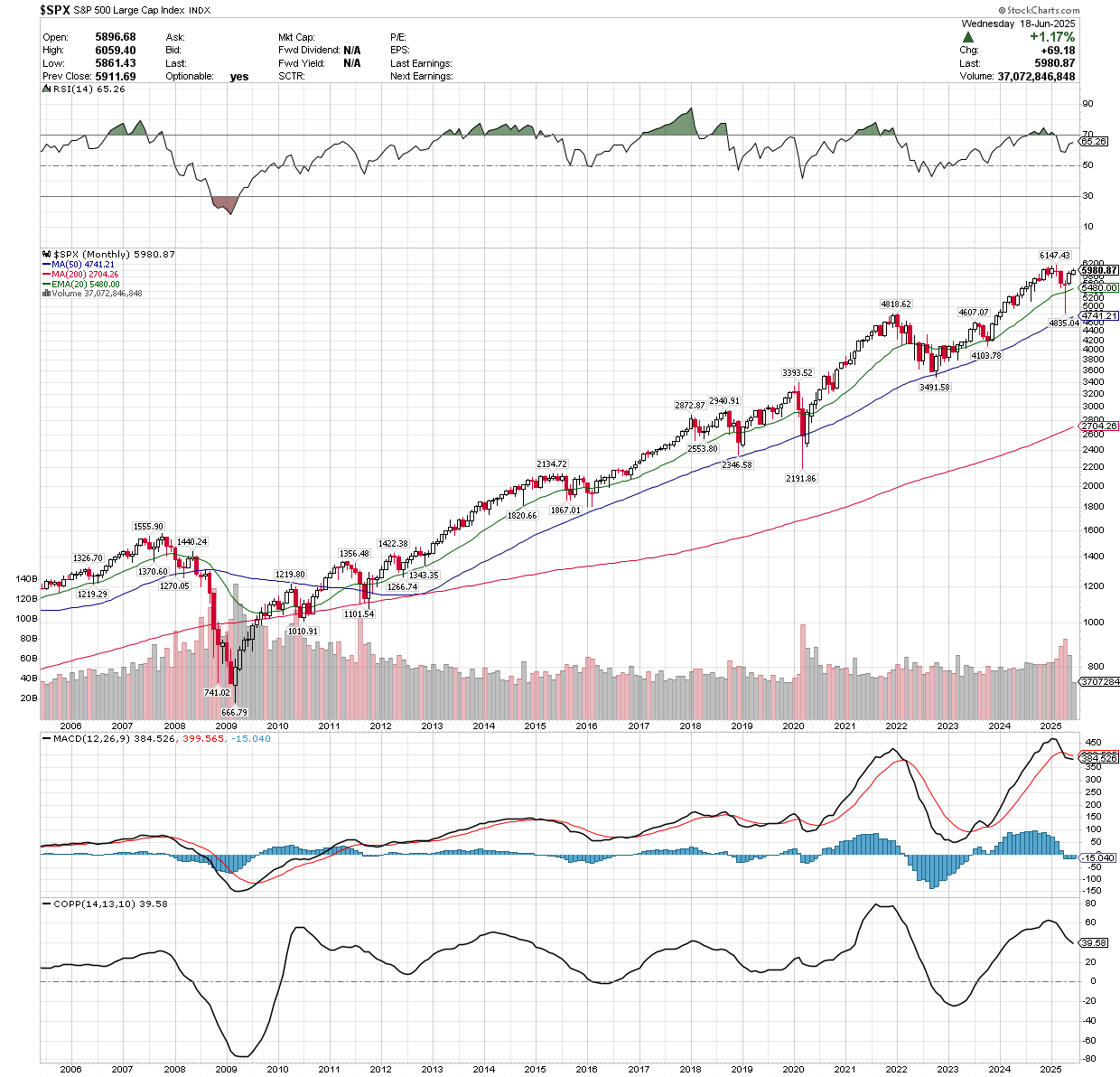

While the short-term picture has been more positive with the strength of this bounce, it has not improved the technical picture of the long-term chart. The indicator that went negative in April remains negative and diverging with price. It also remains at elevated levels indicating it still needs to reset at some point. Ideally, it does so with a high level of consolidation in price and not a sustained breakdown. The long-term uptrend, though, remains intact and the drop in April remained above the blue line. It’s important to note that long-term market tops, historically, are a process and take time. Whether that’s playing out now remains to be seen. The technical signals suggest it is possible but price is not there. As the old saying goes, markets can stay irrational longer than you can stay solvent.

We’ll continue to monitor our indicators and signals to manage risk accordingly. Please reach out with any questions or concerns. We hope everyone has an enjoyable summer and a safe and happy 4th of July!

Cory McPherson is a financial planner and advisor, and President and CEO for ProActive Capital Management, Inc. He is a graduate of Kansas State University with a Bachelor of Science in Business Finance. Cory received his Retirement Income Certified Professional (RICP®) designation from The American College of Financial Services in 2017.

DISCLOSURE

ProActive Capital Management, Inc. (PCM”) is registered with the Securities and Exchange Commission. Such registration does not imply a certain level of skill or training.

The information or position herein may change from time to time without notice, and PCM has no obligation to update this material. The information herein has been provided for illustrative and informational purposes only and is not intended to serve as investment advice or as a recommendation for the purchase or sale of any security. The information herein is not specific to any individual's personal circumstances.

PCM does not provide tax or legal advice. To the extent that any material herein concerns tax or legal matters, such information is not intended to be solely relied upon nor used for the purpose of making tax and/or legal decisions without first seeking independent advice from a tax and/or legal professional.

All investments involve risk, including loss of principal invested. Past performance does not guarantee future performance. This commentary is prepared only for clients whose accounts are managed by our tactical management team at PCM. No strategy can guarantee a profit.

All investment strategies involve risk, including the risk of principal loss.

This commentary is designed to enhance our lines of communication and to provide you with timely, interesting, and thought-provoking information. You are invited and encouraged to respond with any questions or concerns you may have about your investments or just to keep us informed if your goals and objectives change.